Пятьдесят оттенков тирании Центрального банка

Автор: Аарон Дэй Институт Браунстоуна,

У Соединенных Штатов была цифровая валюта Центрального банка (CBDC) с конца 1990-х годов или, возможно, даже с 1970-х годов. Определения имеют значение. Как самый продаваемый роман 50 оттенков серого Изучая сложную динамику контроля и подчинения в отношениях, наша финансовая система превратилась в то, что можно было бы назвать «50 оттенков тирании Центрального банка». "

Каждый слой нашей цифровой валютной системы снимает соблазнительную маску свободы, выявляя все более темные оттенки контроля. По мере того, как мы углубляемся, то, что на первый взгляд кажется автономией, является лишь иллюзией, где скрыты более сложные и распространенные формы доминирования.

Наши политики работают рука об руку, манипулируя самим языком, чтобы создать ложное впечатление, маскируя либо другое намерение, либо просто пытаясь получить видимость победы с небольшими фактическими достижениями или без них. Ведь Патриотический акт был чем угодно, только не «патриотическим». Закон CARES, хотя и звучит горячо чутко, больше заботился о крупных транснациональных корпорациях, чем о малом бизнесе, о Big Pharma над американским здоровьем и, прежде всего, о расширении государства наблюдения и защите цензурного промышленного комплекса над свободой и свободой слова американского народа.

Просто так 50 оттенков серого Раскрывает запутанную игру власти в, казалось бы, согласованных отношениях, так же как и наша нынешняя финансовая система раскрывает свою истинную природу в качестве цифровой доминатрисы, которая неуклонно добавляет связи к цепочке финансового порабощения, ужесточая свою власть над нашей автономией в течение десятилетий.

В этой статье я определю, что такое цифровая валюта Центрального банка, изучив ее основные категории. Я продемонстрирую, что США уже работают с формой CBDC, хотя и без ярких меток. Я также покажу, что Федеральная резервная система (ФРС) может ввести в эту систему более антиутопические элементы, такие как ограничения на программирование, когда, как и где вы можете тратить свои деньги, не требуя одобрения Конгресса.

Тем не менее, страх перед контролем центрального банка над вашими транзакциями на самом деле является «красной серединой». Реальная угроза лежит на нашем правительстве, которое уже усовершенствовало искусство слежки. Добавление программируемости является следующим логическим шагом. В конечном счете, и республиканцы, и демократы направляют нас к одному и тому же пункту назначения: тотальному цифровому контролю. Они могут использовать разные слова и различную пропаганду, но их цели сходятся. Хотя мы не можем просто проголосовать из этого затруднительного положения, мы можем полностью отказаться.

контекст

Если вы следите за мной, вы знаете, что я был сосредоточен на предупреждении людей об угрозах CBDC в течение последних двух лет. Это посвящение привело меня к написанию книги. Последний отсчетИ даже баллотироваться на пост президента, чтобы повысить осведомленность о проблеме. Я передал копию своей книги Вивеку Рамасвами, и после ее прочтения наши разговоры помогли привлечь внимание Дональда Трампа к проблеме CBDC. С тех пор, как я покинул гонку в октябре прошлого года и стал членом Brownstone, я побывал в 22 штатах, чтобы обсудить опасности CBDC.

В настоящее время я провожу более 15 четырехчасовых семинаров по всей стране и вскоре на международном уровне, обучая людей использованию альтернативных валют, чтобы избежать CBDC и уклониться от них. Великое взятиеЭто тщательно разработанный процесс, который может лишить нас наших акций, облигаций и 401 (k)s, чтобы принести пользу крупнейшим банкам посредством юридических маневров во всех 50 штатах.

Я вошел в криптопространство в 2012 году, но только когда я увидел друзей и людей, которыми я восхищался, когда их арестовывали, заключали в тюрьму или уничтожали их предприятия федеральным правительством, я стал по-настоящему увлечен этим вопросом. С тех пор Я покинул свой личный банковский счет в 2019 году, это повлияло на меня лично. Я начал изучать эту тему и обнаружил, что подавление криптовалют напрямую связано с CBDC. Проще говоря, правительству нужно было расправиться с криптовалютой, чтобы открыть CBDC.

В течение двух лет я путешествовал по стране (и вскоре по всему миру), чтобы предупредить людей об опасностях CBDC. Но поскольку я углубился в технические и юридические аспекты этого, я пришел к выводу, что у нас уже есть CBDC. У нас есть десятилетия. Наши транзакции уже проверены. Банки и правительство могут цензурировать наши счета. Деньги на наших банковских счетах уже цифровые (не менее 92%). Нет необходимости беспокоиться о будущей угрозе КБР. Они у нас уже есть. На данный момент мы просто боремся за нашу степень рабства.

Доллар — это просто вход в базу данных.

Становится ясно, что у нас уже есть CBDC, когда вы начинаете изучать, как создаются деньги.

Как было показано в моей предыдущей статье «Вы можете не владеть ничем раньше, чем думаете», современная коммерция теперь проходит через обширные централизованные базы данных. Эти базы данных составляют основу нашей финансовой системы, в которых хранится все, от остатков на наших банковских счетах до наших запасов. Деньги ничем не отличаются.

Начнем с основ создания денег: государственных заимствований. Правительство продает долговые расписки в форме казначейских ценных бумаг (векселей, банкнот и облигаций) Федеральному резерву. Где Федеральная резервная система получает деньги на покупку этих ценных бумаг? Они создают его из воздуха. Или, если быть более точным, в базу данных просто добавляют какие-то единицы и нули — база данных Oracle, не меньше (спасибо, Ларри Эллисон!).

Федеральное правительство затем оплачивает свои счета через свой счет в Федеральной резервной системе. Когда выписывают чеки для проектов, таких как туннель черепах во Флориде стоимостью 3,4 миллиона долларов или исследование на 600 000 долларов о том, почему шимпанзе выбрасывают фекалии, средства переводятся из базы данных Oracle ФРС на счета продавцов и сотрудников коммерческих банков, каждый из которых поддерживает свои собственные отдельные базы данных. Некоторые используют Oracle, другие — Microsoft.

Вот где это становится еще более абсурдным: на каждый доллар, депонированный клиентами, коммерческий банк может создать девять новых долларов в своей базе данных, чтобы кредитовать других клиентов. У нас есть система частичного резервирования, и в течение многих лет (с 1992 года) банки должны были отправлять 10% депозитов обратно в Федеральную резервную систему. Законодательство Covid-19 отменило это требование, и теперь банки не обязаны иметь 10% в Федеральной резервной системе (хотя по ряду других причин они все еще сохраняют этот уровень в ФРС).

Правительство выпускает IOU Федеральной резервной системе, которая создает цифровые деньги в базе данных. Правительство оплачивает свои счета, чеки депонируются в коммерческих банках, которые создают дополнительные деньги, и часть их отправляется обратно в ФРС - все в виде цифровых записей в базах данных. Если вы сложите количество баз данных Центрального банка и Коммерческого банка по всему миру, вы получите более 60 000 отдельных баз данных, отправляющих записи туда и обратно.

Что такое CBDC?

Когда кто-то спрашивает меня: «Что такое CBDC?» Начну с изучения грамматики вопроса. CBDC является цифровой валютой центрального банка. Федеральная резервная система — это наш центральный банк, и наша валюта уже цифровая — 1 и 0 создаются из воздуха в базе данных Oracle. По этому определению, у нас был CBDC в течение десятилетий.

По состоянию на 2024 год только 8% американской валюты существует физически, оставляя остальные 92% цифровыми. Являются ли они 92% CBDC? Мы становимся CBDC в тот момент, когда более 50% нашей валюты существует в цифровом виде.

Политики и центральные банки утверждают, что в настоящее время у нас нет CBDC, и вряд ли согласятся с моим определением. Я попытался понять их определения и изолировать расхождения.

Вообще говоря, когда центральные банки, Всемирный экономический форум (ВЭФ), Организация Объединенных Наций (ООН), Всемирный банк, Международный валютный фонд (МВФ) и Банк международных расчетов (БМР) говорят о CBDC, по своей сути, они определяются как цифровые, являющиеся ответственностью центрального банка (в отличие от ответственности коммерческих банков), и, если вы помните ранее, создайте свои собственные деньги в своей отдельной базе данных и предоставьте только небольшую сумму (10%) обратно центральному банку в виде резервов.

Это всегда казалось мне разницей без различия. Почему? Потому что именно коммерческие банки владеют Федеральной резервной системой — или, по крайней мере, таково общее мнение. Как частное лицо, истинная собственность Федеральной резервной системы по-прежнему окутана тайной, но, судя по всему, она контролируется картелем частных банков. Я рекомендую книгу Г. Эдварда Гриффина. Существо с острова Джекилл для более глубокого понимания этого.

Вот как это работает: Деньги изначально создаются в базе данных Федеральной резервной системы, а затем депонируются в отдельные базы данных тех самых банков, которые владеют Федеральной резервной системой. Эти банки, в свою очередь, создают еще больше денег на основе этих депозитов.

Отказавшись от идеи, что валюта, выпущенная центральным банком, и валюта, выпущенная центральным банком, которая затем используется в качестве поддержки для выпуска большего количества валюты коммерческим банком, фактически получают то же самое, учитывая, что банки владеют Федеральной резервной системой, давайте рассмотрим некоторые другие заблуждения о CBDC.

Миф: Если у меня есть CBDC, у меня будет счет непосредственно в Федеральной резервной системе, и мой банк исчезнет.

Большинство людей опасаются, что цифровая валюта центрального банка означает, что они будут иметь счет непосредственно в Федеральной резервной системе, а коммерческие банки исчезнут. Это также одна из причин, по которой многие считают, что CBDC никогда не произойдет, потому что коммерческие банки будут сопротивляться и бороться до смерти за свое выживание. Однако ни одна из запущенных CBDC (включая китайскую) не имеет такой структуры. В Китае Народный банк Китая (НБК) создает CBDC, а затем выдает его коммерческим банкам.

Потребители не имеют прямого отношения к центральному банку. Есть 134 страны, которые стремятся получить CBDC, и мы не видели, чтобы кто-либо (в том числе США) рассматривал возможность сокращения коммерческих банков. Поэтому я не думаю, что вы можете разумно сказать, что потребители, имеющие счет непосредственно в центральном банке, являются критическим требованием для того, чтобы быть CBDC.

Когда вы слышите, как говорящие головы из ООН, ВЭФ, Всемирного банка, МВФ и других говорят о CBDC, вы часто слышите о программируемости, надзоре и контроле, финансовой интеграции и основных элементах. Давайте проведем тест и посмотрим, имеет ли нынешний доллар или может иметь эти «особенности». "

Программируемость:Самые антиутопические опасения по поводу CBDC связаны с их способностью программироваться. Теоретически, с их туманными владельцами, правительствами или центральными банками можно внедрить правила, диктующие, как, когда, где и даже если вы можете потратить свои цифровые деньги. Люди часто связывают эту программируемость с блокчейн-технологиями, такими как Биткойн и Эфириум, с использованием смарт-контрактов и токенов (уникальные цифровые представления активов, которые я подробно обсуждаю в этой статье).

Вам не нужна новая технология блокчейн для программирования. База данных Oracle Федеральной резервной системы, а также системы Microsoft и Oracle, используемые коммерческими банками, программируются прямо сейчас. Компании и частные лица используют интерфейсы прикладного программирования (API) с этими базами данных в течение многих лет. Уже существуют правила для обозначения определенных транзакций, основанные на конкретных критериях, а именно, что такое программируемость. Таким образом, хотя наличие единой централизованной цифровой валюты может облегчить для Большого Брата соблюдение правил расходов, технология для этого уже жива и работает в нашей нынешней системе.

Существующая финансовая система в значительной степени зависит от сложных алгоритмов и автоматизированных процессов принятия решений, влияющих на все, от обработки платежей до оценки кредитоспособности. Но что действительно удивительно, так это степень, в которой программирование уже проникло в нашу финансовую жизнь, с примерами, включая кредитные карты, которые могут отключить доступ к деньгам на основе выбросов углерода, сберегательные счета для здоровья, которые позволяют покупать только предварительно одобренные медицинские расходы, алгоритмы маршрутизации транзакций, которые отдают приоритет определенным продавцам над другими, системы борьбы с отмыванием денег, которые отмечают подозрительную активность в режиме реального времени, и платежные процессоры, которые могут динамически корректировать процентные ставки и сборы на основе индивидуальных кредитных баллов.

Сложная серия алгоритмов и автоматизированных процессов принятия решений уже работает, когда вы отправляетесь в магазин товаров для дома, чтобы купить новую газовую плиту. Когда вы прокручиваете свою кредитную карту, чтобы совершить покупку, алгоритм платежного процессора проверяет ваш кредитный рейтинг, чтобы определить, имеете ли вы право на покупку, в то время как система банка проверяет баланс вашего счета, чтобы убедиться, что у вас достаточно средств для покрытия транзакции.

Между тем, система борьбы с отмыванием денег (AML) работает в фоновом режиме, отмечая любую подозрительную деятельность, которая может указывать на отмывание денег или другую незаконную деятельность. Алгоритм также проверяет код категории продавца (MCC) для магазина товаров для дома, проверяет, что покупка находится в пределах утвержденных вами лимитов расходов, и рассчитывает процентную ставку и сборы, связанные с вашей кредитной картой, на основе вашего индивидуального кредитного рейтинга. По мере обработки транзакции алгоритм платежного процессора направляет платеж в банк магазина, и средства перечисляются, все в считанные секунды, что позволяет вам забрать новую газовую плиту домой и начать готовить бурю.

Doconomy Mastercard, ко-брендовая карта Организации Объединенных Наций, делает еще один шаг вперед, связывая финансовые операции с выбросами углерода. Карта использует алгоритмы для отслеживания углеродного следа каждой покупки, и если расходы пользователя на углерод превышают определенный предел, карта может быть отклонена или даже отключена. Эта социальная инженерия достигается через сложную систему, которая присваивает углеродный балл каждому торговцу и транзакции, учитывая такие факторы, как тип приобретаемых товаров или услуг, местоположение и используемый способ транспортировки. Затем алгоритм вычисляет общий углеродный след пользователя и сравнивает его с заданным пределом, который может быть скорректирован на основе индивидуального углеродного бюджета пользователя. Если лимит превышен, карта может быть ограничена или выключена, ограничивая доступ пользователя к своим деньгам.

Сберегательные счета (HSA) являются еще одним примером программируемости в финансовой системе. HSA - это сберегательные счета с налоговыми льготами, которые позволяют людям выделять средства на медицинские расходы. Тем не менее, эти учетные записи имеют строгие правила и ограничения на то, какие продукты и услуги могут быть приобретены. Средства в HSA могут использоваться только для предварительно утвержденных расходов на здравоохранение, таких как визиты к врачу, рецепты и медицинское оборудование.

Счет связан с дебетовой картой или чековой книжкой, но средства могут использоваться только у продавцов, которые были предварительно одобрены администратором HSA. Это достигается с помощью системы кодов торговых категорий (MCC), определяющих тип бизнеса или предоставляемых услуг. Когда карта HSA прокручивается, MCC проверяется по списку утвержденных кодов, чтобы гарантировать, что транзакция имеет право на возмещение. Если MCC не одобрена, транзакция отклоняется, что ограничивает возможность доступа пользователя к собственным средствам для немедицинских расходов. Эта программируемость гарантирует, что средства HSA используются только по назначению, обеспечивая при этом удобный и эффективный способ экономии на медицинских расходах.

Когда политик произносит речь, утверждая, что они ведут хорошую борьбу с этими ужасными CBDC на основе защиты американцев от того, чтобы их деньги были запрограммированы, сообщите им о том, как работает существующая система. Никаких серьезных технических обновлений не требуется, и не было принято никаких значительных законов, чтобы добавить больше программируемости. Новые правила и алгоритмы разрабатываются каждый день, без каких-либо публичных слушаний, одобрения Конгресса или даже крика на вашем любимом канале финансовых новостей.

Наблюдение:Если и есть одна вещь, о которой американцы все больше беспокоятся, так это то, что каждая сделка будет находиться под пристальным вниманием правительства. Тед Круз сказал: «Администрация Байдена активно работает над созданием новой цифровой валюты, которая позволит правительству шпионить за нашими транзакциями и контролировать нашу финансовую свободу. Мы должны прекратить это сейчас». Рон ДеСантис также сделал свою позицию предельно ясной, заявив: «Толчок администрации Байдена к созданию цифровой валюты Центрального банка связан с наблюдением и контролем. Флорида этого не выдержит, мы будем защищать финансовую конфиденциальность и безопасность жителей Флориды. "

И давайте не будем забывать сенатора Синтию Луммис, республиканского сенатора Вайоминга, которая является фаворитом среди энтузиастов биткоина. Она также подняла тревогу: «Я глубоко обеспокоена стремлением администрации Байдена создать КБР. Его можно использовать для сбора информации об американцах и, возможно, даже для контроля за их расходами. Мы должны обеспечить, чтобы любая цифровая валютная система защищала конфиденциальность и личную свободу. "

Это не просто республиканцы размахивают флагом, блеют о конфиденциальности. Даже Элизабет Уоррен, которая выступала за CBDC, сказала: «Если мы собираемся создать цифровой доллар, мы должны убедиться, что он работает для всех, а не только для богатых, и что он защищает конфиденциальность потребителей. "

Как благородно. Как патриотично. Насколько они оторваны от реальности своих голосов. Наш текущий цифровой доллар отслеживается и подвергается цензуре на протяжении десятилетий.

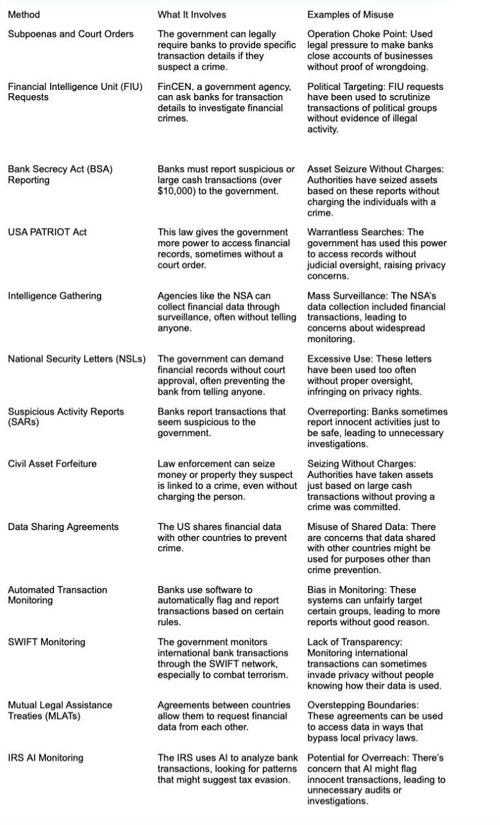

В США правительство имеет различные методы получения доступа к информации о финансовых транзакциях, в зависимости от типа информации и обстоятельств. Вот некоторые из их методов:

Давайте обсудим это в более личных терминах. Я мог бы написать целую книгу с простыми примерами того, как правительство использовало методы наблюдения для нацеливания на людей. У меня есть друзья в тюрьме за ненасильственные преступления, ставшие возможными благодаря этой самой слежке.

Я выбрал эти два драгоценных камня, потому что они подчеркивают, насколько экстремальны меры надзора в нашей банковской системе, как это происходит сегодня.

Дело Ребекки Браун: конфискация гражданских активов ошиблась

В 2015 году отец Ребекки Браун, Терри Браун, ехал из своего дома в Мичигане, чтобы навестить семью в Нью-Джерси. У него было 91 800 долларов наличными, и его дочь потратила годы на покупку дома. Терри не доверял банкам (мудрый человек), поэтому он отозвал деньги и взял их с собой на хранение.

Во время поездки по Пенсильвании полицейский штата остановил его за незначительное нарушение правил дорожного движения. Когда офицер обнаружил наличные, он сразу же стал подозрителен, несмотря на четкое объяснение Терри, что деньги принадлежали его дочери и предназначались для покупки дома. Без каких-либо обвинений или доказательств преступления полиция изъяла все 91 800 долларов в соответствии с законами о конфискации гражданских активов.

Ребекка и ее отец потратили более года и тысячи долларов, пытаясь вернуть свои деньги. Это дело привлекло национальное внимание, подчеркнув оскорбительный характер законов о конфискации гражданских активов, которые позволяют правоохранительным органам брать деньги у невинных людей без каких-либо доказательств правонарушений. В конце концов, деньги были возвращены, но только после долгой и дорогостоящей юридической битвы, которая оставила семью финансово напряженной и эмоционально истощенной.

История Ника Меррилла: Скриншоты из National Security Letter

Ник Меррилл владел небольшим интернет-провайдером в Нью-Йорке. Однажды в 2004 году его жизнь полностью изменилась, когда ФБР вручило ему письмо национальной безопасности. Письмо требовало, чтобы он передал конфиденциальные записи клиентов, и оно пришло с заказом на кляп. Ему не разрешалось никому, в том числе его адвокату, сообщать о запросе.

Меррилл был в ужасе. ФБР не предоставило никаких доказательств или судебного приказа — только NSL. Он не мог оспорить письмо в суде, потому что приказ о рвоте сделал незаконным говорить об этом. Меррилл чувствовал, что его конституционные права были нарушены, но не имел видимых средств правовой защиты.

В течение многих лет Меррилл боролся с приказом о кляпах втайне, не в состоянии рассказать даже своим ближайшим друзьям, что происходит. Только в 2010 году, шесть лет спустя, Меррилл наконец-то получил право публично говорить о своем деле, став первым человеком, который успешно оспорил приказ о запрете NSL. Опыт оставил его глубоко потрясенным. И поскольку он был первым, кто успешно бросил вызов NSL, мы не знаем, сколько людей имели подобный опыт.

Итак, позвольте мне перечислить это для вас: АНБ уже массово собирает наши финансовые данные, Налоговое управление США (IRS) использует ИИ в сочетании с Налоговым управлением США (IRS) для мониторинга наших расходов, у банков уже есть правила (программирование) для отслеживания подозрительного поведения, и между Патриотическим актом и Письмами национальной безопасности мы можем шпионить без одобрения суда и, возможно, даже не сможем говорить об этом (даже с адвокатом).

Наши деньги являются цифровыми, и они уже находятся под строгим наблюдением. Насколько хуже может быть? Сначала я подумал, что, может быть, такие люди, как Круз, ДеСантис и Уоррен, не понимают, насколько глубока уже кроличья нора наблюдения. Но потом я копнул глубже. Несмотря на публичный протест по поводу неприкосновенности частной жизни, Тед Круз проголосовал за Закон о свободе США, который повторно санкционировал части Патриотического акта, включая эти надоедливые NSL. Уоррен тоже поддержал его, настаивая на усилении Закона о банковской тайне. Он голосовал за Закон о свободе США и поддерживал усилия по ужесточению контроля над Законом о банковской тайне.

Финансовая интеграция: Одно из самых абсурдных утверждений и идеальная демонстрация оруэлловского двойного слова от глобалистских организаций, таких как ВЭФ, ООН и Банк международных расчетов, заключается в том, что CBDC будут способствовать финансовой интеграции.

Когда они говорят CBDC, они имеют в виду запрет на физические деньги. Помните, что ни одно формальное определение не говорит о том, что вы не можете иметь CBDC наряду с физическими деньгами. Само определение CBDC не только оспаривается между этими группами, но и смещается и становится более узким с течением времени. Отчасти я думаю, что это отклоняется от того, насколько авторитарна уже существующая система. У вас могут быть как наличные, так и CBDC, как мы уже делаем в Америке, и многие другие пилотные программы по всему миру предполагают либо наличие физических наличных денег вместе с CBDC, либо постепенное прекращение наличных. Опять же, определения имеют значение. Включение BIS и WEF означает, что они будут лишать деньги и называть это прогрессом.

Вот кикер: около 4,5% американцев не имеют банковских счетов и зависят от физических денег, чтобы выжить. В системе CBDC использование системы и проведение транзакций требуют разрешения, и это разрешение может быть отказано. Банки могли бы полностью исключить этих людей из экономики, оставшись без каких-либо средств обмена. Это не включение, это хуже, чем нынешняя ситуация. Это явное исключение.

Токенизация:МВФ и БМР продвигают семантический аргумент о том, что цифровая валюта центрального банка (CBDC) является действительно «цифровой», только если она токенизирована, то есть присвоена уникальная, отслеживаемая валюта каждой единице валюты. Однако это различие в значительной степени связано с терминологией, а не с содержанием. Подавляющее большинство денег уже существует в цифровой форме, хранится в базах данных, таких как база данных Oracle Федеральной резервной системы или базы данных Oracle / Microsoft коммерческих банков. Реальная дискуссия не о том, являются ли деньги цифровыми, а о том, кто контролирует цифровую книгу. В США разделение, похоже, идет по партийной линии, при этом демократы выступают за токенизированную валюту, выпущенную центральным банком, в то время как республиканцы во главе с Синтией Луммис настаивают на выпуске стейблкоинов коммерческими банками. Однако это различие должно быть более точным, поскольку оба варианта в равной степени программируемы, контролируются и контролируются правительством.

Кроме того, коммерческие банки владеют центральными банками, что делает различие между ними спорным. Токенизация не делает что-то «цифровым», это просто другой тип цифрового представления. В конечном счете, будь то токен, выпущенный центральным банком, или стейблкоин, выпущенный коммерческим банком, результатом является программируемая, отслеживаемая и потенциально угнетающая цифровая валюта, угрожающая индивидуальной свободе и автономии.

CBDC Наконец-то определен

У нас есть цифровая валюта центрального банка. Политики и глобалистские организации, такие как ООН/ВЭФ/БМР, любят менять целевые позиции, добавляя узкие определения, которые становятся более тираническими с каждым новым переопределением.

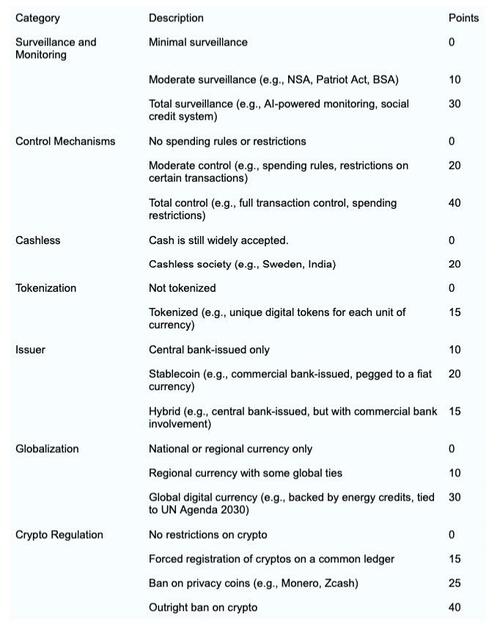

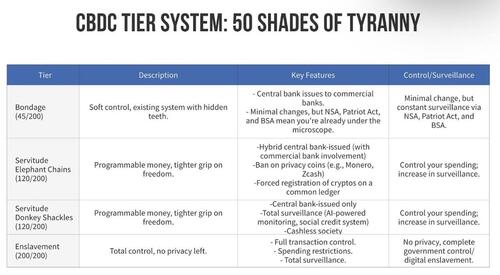

Цифровые валюты Центрального банка (ЦБДК) уже не концепция будущего, а реальность настоящего. Мы не ждем их реализации, они уже здесь, и теперь мы измеряем степени тирании, которые приходят с ними. Индекс тирании CBDC — это инструмент, который помогает нам понять уровень контроля и наблюдения, который приходит с этими цифровыми валютами.

Вместо того, чтобы позволить им сформулировать дебаты, добавив новые колокола и свистки в определение CBDC, я создал индекс, выпущенный как система подсчета очков, чтобы определить уровень тирании. Индекс состоит из нескольких категорий: наблюдение и мониторинг, механизмы контроля, безналичное общество, токенизация, эмитент, глобализация и крипторегулирование. Каждая категория имеет балл, и сумма этих баллов указывает на уровень тирании. Чем выше балл, тем более угнетающим является CBDC.

Мы уже находимся на уровне Бондажа с оценкой, которая указывает на значительную потерю свободы и автономии. Но это не остановится на этом. Отсечение для уровня сервитута составляет 120 пунктов, и есть несколько способов достичь этого порога. Одним из способов является более широкое использование мониторинга на основе ИИ в сочетании с безналичным обществом и токенизацией. Но не заблуждайтесь: это всего лишь один из возможных путей к рабству. Мы знаем конец игры: глобальная цифровая валюта привязана к системе социального кредита, где каждая транзакция отслеживается и контролируется. Это антиутопическое будущее, которое обсуждается в моей книге. Последний отсчет.

Как мы можем дать отпор

Я написал эту статью, чтобы прояснить одну вещь: у нас уже есть CBDC. CBDC — это не угроза будущего, это реальность. Существующая система уже цифровая, программируемая и отслеживаемая. Политики, центральные банкиры и глобалистские организации продолжают менять определение CBDC, чтобы отвлечься от того факта, что у нас уже есть один, и подготовить нас к еще более глубоким оттенкам тирании.

Мы должны взять на себя ответственность за определение CBDC, чтобы прояснить их намерения, то есть они движутся к абсолютному цифровому порабощению и глобальной технократии.

Мы должны забить и мемить оковы, рабство и порабощение уровней CBDC и объяснить различные элементы индекса тирании CBDC. Мы должны привлечь внимание к тому факту, что республиканцы и демократы являются соучастниками в осуществлении этой тирании, оба соучастниками семантических манипуляций с определением CBDC, и оба активно работают над принятием законодательства, которое повышает уровень тирании от рабства до рабства.

Демократы доведут нас до уровня рабства через выпущенный Центральным банком токенизированный доллар под видом финансовой интеграции. Такова нынешняя политика в соответствии с указом президента Байдена 14067. Республиканцы доставят нас туда путем усиленного наблюдения и предоставления монопольного контроля над цифровой валютой токенизированных коммерческих банков крупнейшим банкам, скорее всего, под видом прекращения незаконной иммиграции, терроризма и отмывания денег.

Я подчеркиваю поведение политиков по обе стороны прохода, а не потому, что я думаю, что вы должны писать или звонить своему конгрессмену. Мы не можем голосовать за свой выход. Все законы, которые добавили программируемость и слежку, были двухпартийными. Каждая фиатная валюта в истории человечества потерпела неудачу, и даже последние 5 мировых резервных валют длились всего 84 года. Разница на этот раз в том, что это контролируемый снос. Они делают это намеренно, чтобы создать полностью цифровую систему управления.

Путь вперед лежит через радикальное несоблюдение и принятие монетарных альтернатив, которые находятся вне контроля государства. В 2019 году я перестал пользоваться личным банковским счетом и начал пользоваться криптовалютами, золотом и серебром. В свете недавних откровений об угоне биткоина (рекомендую к прочтению) Угон Bitcoin Для получения дополнительной информации) и его прослеживаемости я перешел на монеты конфиденциальности, такие как Zano и Monero, а также использую физическое золото, золотые спинки и серебро. В настоящее время я провожу 4-часовые семинары в городах по всей территории США и вскоре на международном уровне, где я показываю людям, как получить и использовать альтернативные валюты в качестве замены доллару. .

Выходя из доллара сейчас, мы можем положить конец нашему рабству, предотвратить полное цифровое порабощение и построить будущее, основанное на свободной воле и централизации. Мы не должны жаловаться на потерю нашей нынешней системы. Мы должны разжечь слезы и начать более свободное, децентрализованное будущее.

Тайлер Дерден

Сат, 08/31/2024 - 16:00

![Krok po kroku wali się kamienica w centrum Świdnicy. Nadzór budowlany zawiadamia prokuraturę [FOTO]](https://swidnica24.pl/wp-content/uploads/2026/05/Pulaskiego-14-kamienica-2026.05.23-5.jpg)