Рынок RINO: рецессия только по названию ?

ИПЦ завершен? Проверь!

ATH Equity? Проверь!

Американские фондовые рынки остаются устойчивыми, подкрепленными сильными перекрестными потоками активов.

Митинг, похоже, продлится до Дня труда. за рулем:

Надежная корпоративная прибыль в целом превышает ожидания

Разнообразное участие корпораций, учреждений и розничных инвесторов

Концентрированное лидерство в области ИИ, большой капитализации, качества и технических названий

Тем не менее, импульс может исчезнуть в сентябре. исторически самый слабый месяц на фоне сезонности и возобновления взаимодействия с инвесторами после лета.

Как теперь объясняет Скотт Рубнер (бывший гуру Goldman) со своего места в Citadel Securities: Это рынок #RINO, рецессия только по названию....

I. Citadel Securities On-the-Ground Sentiment

Активность клиентов остается на рекордно высоком уровне на фондовом рынке:

Денежные акции: Розничные чистые покупатели 15 из последних 17 недель

Розничные варианты: 15-недельная серия покупок16 из последних 17 недель

Институциональные варианты: Бычий тон в 5 из последних 6 недель

Второй. Стратегические дебаты на этой неделе: когда деньги возвращаются в активы риска?

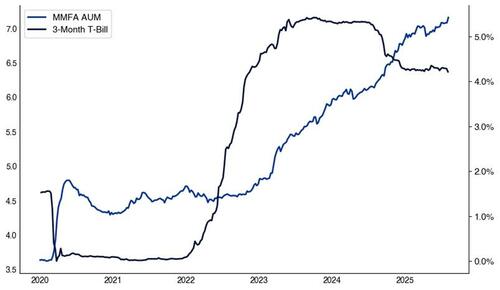

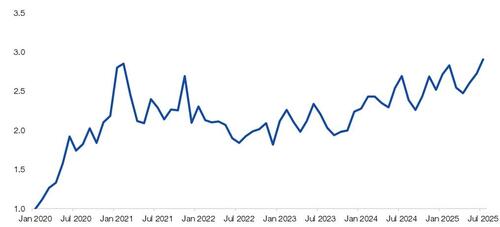

Поскольку ICI отчитывается о денежном рынке AUM на уровне $7,15 трлн (по сравнению с $3,63 трлн в начале 2020 года), ключевым вопросом становится: какой уровень доходности будет стимулировать перераспределение в рисковые активы, если ФРС изменит политику?

Сдвиг в 10% (~ $700 млрд) может активизировать акции, приносящие дивиденды, высококачественный кредит и рисковые активы, такие как «эффект января» (сезонная аномалия, когда акции имеют тенденцию к росту).

Q4 Вращение Смотри: По мере того, как ожидания по ставкам смягчаются, этот «сухой порошок» может привести к росту следующих 493 акций в S&P 500.

Активы денежного рынка (триллион) против США 3-месячная доходность денежного рынка (%)

Январь 2020 — август 2025

Источник: ICI, как сообщает Bloomberg и составляется Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

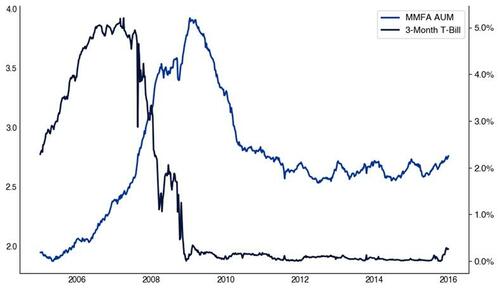

Исторический аналог: В 2010 году активы денежного рынка упали на 27% по мере снижения доходности, предшествуя ротации на акции.

Активы денежного рынка (триллион) против США 3-месячная доходность денежного рынка (%)

Январь 2005 — январь 2015

Источник: ICI, как сообщает Bloomberg и составляется Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

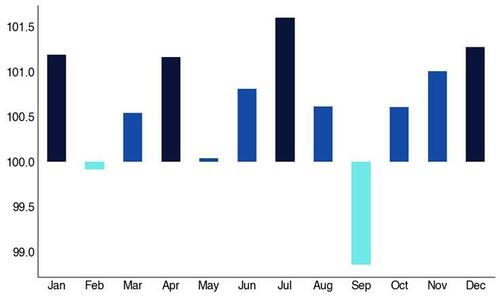

III. Сезонные часы

Сентябрьская настройка

3 сентября часто отмечается месячный максимум для SPX с 1928 года.

День после работы Участие в FOMO обычно исчезает, ограничивая поведение покупки.

SPX и NDX исторически показывают силу августа, за которой следует слабость сентября.

SPX 500 Ежемесячное исполнение

1928 - Сегодня

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

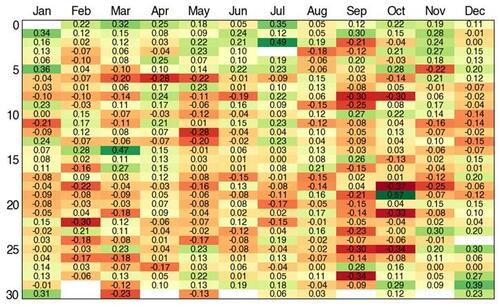

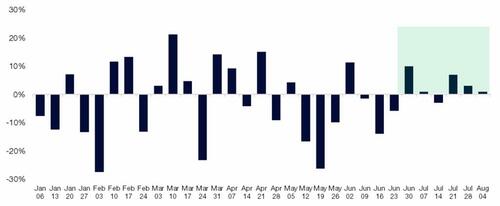

SPX 500 Daily Performance Quilt

1928 - Сегодня

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

IV. Розничная позиционирование

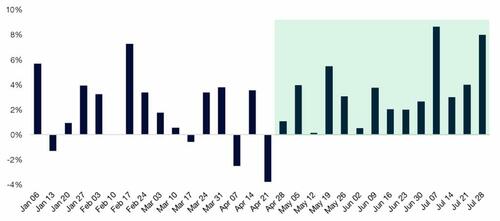

1. Розничные денежные акции Citadel Securities: Чистые покупатели в 15 из последних 17 недель, После мягкого апреля.

Розничные денежные акции - чистое понятие по неделям

Звук Dev January - август 2025

Источник: Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

2. Текущая сила с 19 месяцами чистого условного и покупки акций.

3. Динамика сезонности розничных денежных средств Citadel Securities основана на данных за август 2017 года - июль 2025 года.

Июнь и июль = Сильный

Август - медленнее

Сентябрь - самый слабый

Розничная наличность - доля чистой номинальной по месяцам

1 августа 2017 — 31 июля 2025

Источник: Citadel Securities, по состоянию на 8/5/25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

V. Волатильность и позиционирование вариантов

4. Розничные опции Июль 2025 года установил новый ежемесячный рекорд по объему в Citadel Securities.

Розничные опционы - среднесуточный объем по месяцам

Нормализовано до января 2020 года

Источник: Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

5. Citadel Securities покупает Streak

15-недельная серия покупок и 25 из последних 27 торговых дней.

Пятничная активность достигла 99-го процентиля, что на 41% выше 12-месячного показателя.

Розничные опции - Put / Call Direction Соотношение по неделям

Январь-июль 2025

Источник: Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

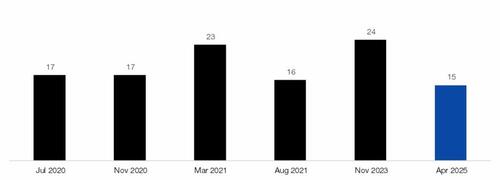

6. Бычьи розничные опционы Citadel Securities Streak Watch

6-я самая длинная серия бычьих опционов с 2020 года

Средняя продолжительность топ-5 полос составляет 18 недель Комната для рабочего дня вверх ногами?

Самый длинный розничный еженедельный опцион на покупку полос на рекорде с 2020 года.

# недели

Источник: Citadel Securities, по состоянию на 8/5/25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

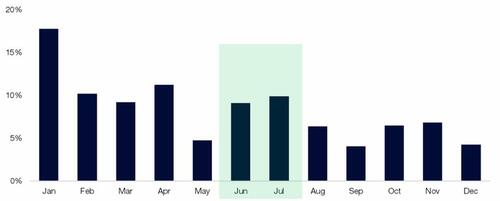

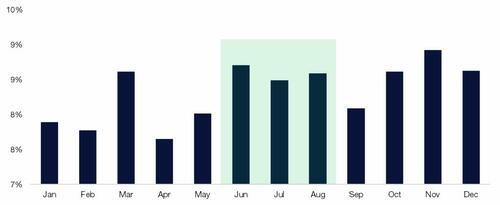

7. Сезонное падение впереди?

Объем розничных опционов Citadel Securities обычно уменьшается в сентябре.

Розничные опционы - Доля объема контракта по месяцам

Январь 2020 — декабрь 2024

Источник: Citadel Securities, по состоянию на 8/5/25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

8. Citadel Securities институциональные опционы

Бычьи 5 из последних 6 недель, достигая пика в 89-й процентиль. Обратите внимание, что клиенты Institutional Options перешли с медвежьего на бычье в прошлом месяце.

Институциональные опционы - Коэффициент направления вызова/запуска по неделям

Январь-август 2025

Источник: Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

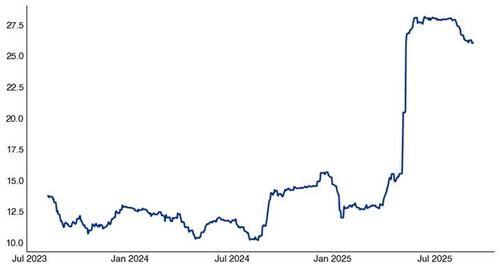

9. Тенденция волатильности: Реализованный vol продолжает падать. VIX на момент набора текста = 15.20

3 месяца: 26

1 месяц: 9

1 неделя: 12

SPX 3-месячная волатильность

Август 2023 — август 2025

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

VI. Корпоративная прибыль и пассивная динамика потока

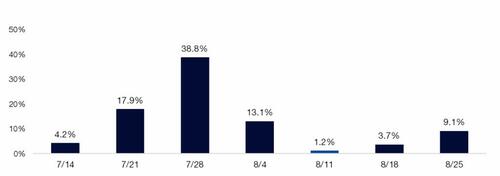

10. Q2 Прибыль: 75,2% рыночной капитализации SPX.

SPX рынок Отчетность за неделю

Q2 Заработок

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 8/5/25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

11. Рост корпоративных выкупов

По данным Birinyi Associates, американские корпорации объявили о разрешении YTD на сумму 983 миллиарда долларов, что делает его лучшим началом года в истории. Кроме того, темпы корпоративных казней составляют 1,1 триллиона долларов, что также установило бы рекорд.

Американские компании объявили о выкупе акций на общую сумму $166 млрд в прошлом месяце, что является самым высоким значением доллара за июль. Предыдущий рекорд составлял 88 миллиардов долларов в июле 2006 года.

12. 2025. Корпоративный Ежедневный поток математика$1,1 трлн за 251 торговый день $4,4 млрд в день Спрос на акции, по данным Birinyi Associates. Август исторически является одним из лучших месяцев года для казней.

13. Отраслевая отчетность завершается, заканчивая Nvidia 8/27.

Сектор SPX GICS по рыночной капитализации

График отчетности о доходах

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

14. Q2 EPS Рост: +11,4% против 5% - самый сильный с 2 квартала 2021 года

- По данным Bloomberg, показатель EPS Q2 на 81% превышает средний показатель за 10 лет в 74%.

SPX Отчетность о доходах

По состоянию на 12 августа 2025 года

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

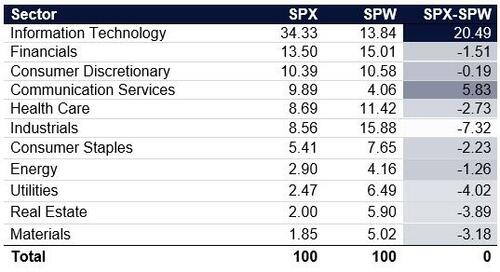

Оригинальное название: Concentration = Прибыль бьет → пассивные притоки → ценовой импульс.

Секторальная концентрация Наблюдения:

Вот 11 секторов S&P 500 GIC для индекса рыночной капитализации S&P 500 («SPX») и равновзвешенного индекса S&P 500 («SPW»).

Технический взвешивание в SPX34,3% против 13,8% в SPW +20,5% распространение

11 секторов S&P 500 по рыночной капитализации SPX %:

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

Эта концентрация усиливает пассивные потоки в более узкую полосу акций; это приводит к «Великолепному 7» против оставшихся 493.

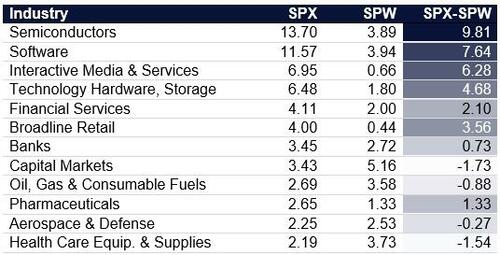

Полупроводники: 13,7% (SPX) против 3,9% (SPW)

Программное обеспечение: 11,6% (SPX) против 3,9% (SPW)

? Эта узкая широта в топовых названиях, создала более частые ветры и сдавливает короткую ногу парной торговли.

Топ-12 отраслей S&P 500 GIC по рыночной капитализации SPX %:

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

15. Август Позитивная политика

Пик S&P 500 приходится на 3 сентября 1928 года.

Последняя неделя августа часто совпадает с низким позиционированием из-за отпусков, вечеринок BBQ, что способствует дрейфу вверх в акциях, особенно в условиях низкого объема.

SPX Август Daily Performance

С 1928 года

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 8/5/25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

NDX Август Daily Performance

С 1985 года

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 8/5/25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

VII. Институциональное позиционирование и систематическое повторное использование

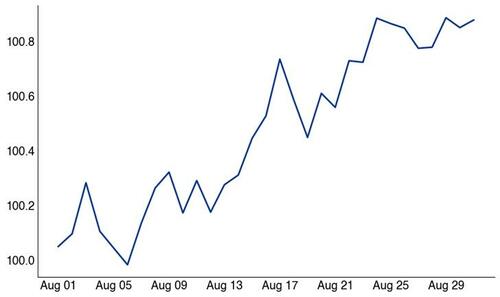

16. CTA: Мы оцениваем, что последователи тренда в настоящее время почти полностью раскрыты в конце августа. предлагатьограниченный постепенный рост. Наша модель показывает, что эта когорта больше не добавляет экспозиции на текущих уровнях.

Акционерное общество США CTA позиционирование

Январь 2024 — июль 2025

Источник: Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

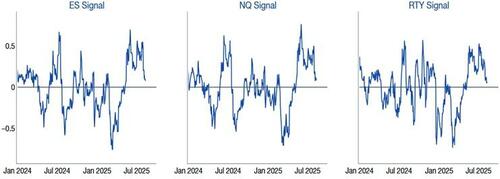

US CTA сигналы

Январь 2024 — июль 2025

Источник: Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

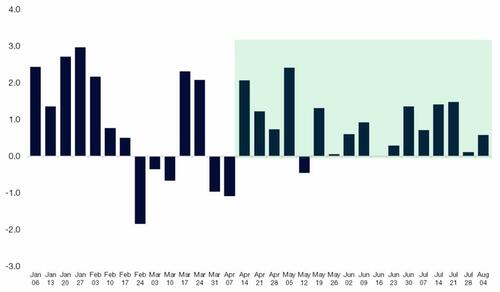

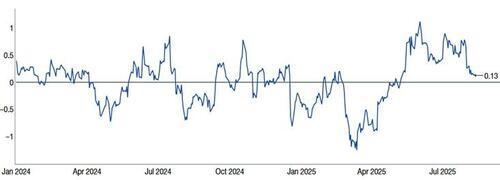

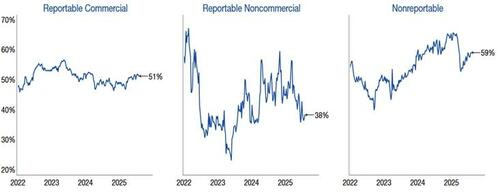

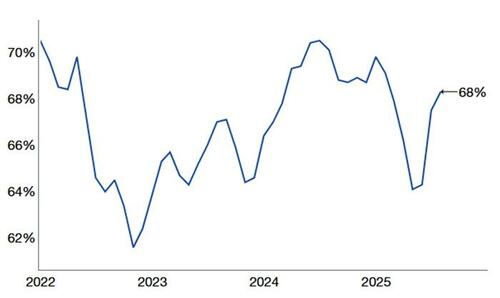

17. CFTC Чистая длинаПродолжается рост позиционирования до исторического уровня.

CFTC S&P 500 консолидированный % Long

Январь 2022 — июль 2025

Источник: COT report, as compiled by Citadel Securities, as of 8/11/25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

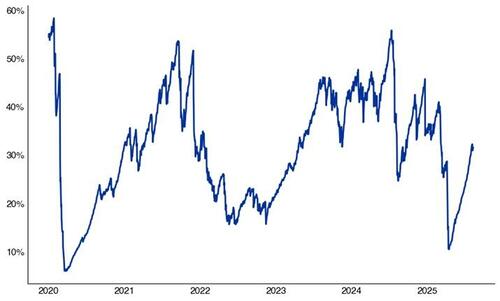

18. Стратегии Vol-Control, которые принимают сигналы от реализованного рынка волатильности, уже значительно увеличили воздействие.

Целевой уровень риска 5%: 32% (по сравнению с 10% в апреле)

Цель экспозиции с 5% контролем риска

Уровень экспозиции с 2020 года

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

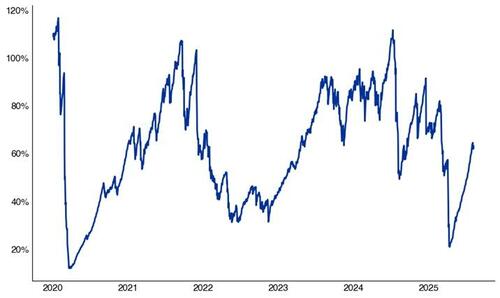

19. Целевая стратегия волатильности 10% в настоящее время подвержена воздействию 63% (по сравнению с 20% в апреле)

Цель экспозиции с 10% контролем риска

Уровень экспозиции с 2020 года

Источник: Bloomberg, составленный Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

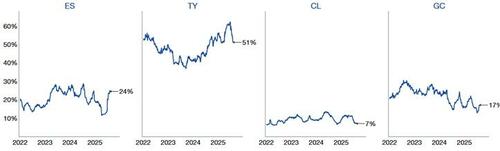

20. Стратегии паритета рисков, обусловленные волатильностью кросс-активов, в настоящее время удерживают экспозицию акций вблизи их 3-летнего среднего уровня в 25%.

Систематическое позиционирование остается повышенным → следите за движениями волатильности, так как перекосы потоков движутся вниз.

Воздействие паритета риска

Январь 2022 - июль 2025

Источник: Citadel Securities, по состоянию на 8/5/25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

21. Нормализация чувствAAII распределяет обратно к историческим средним значениям → меньше по сравнению с одними только настроениями.

Распределение запасов AAII (%)

Январь 2022 - июль 2025

Источник: AAII, как сообщает Bloomberg и составляется Citadel Securities, по состоянию на 12.08.25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

GMI - сентябрьский тактический контрольный список

Системные стратегии (CTA/Vol-Control) при максимальном воздействии Заголовок и экономические риски

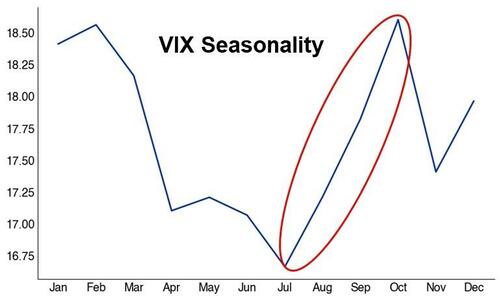

Сентябрь - самый слабый месяц SPX (с 1928)

Волатильность растет Исторически в сентябре (с 1990 года)

VIX Августовское ежемесячное выступление

С 1990 года

Источник: Citadel Securities, по состоянию на 8/5/25. Цифры приведены только для иллюстративных целей. Прошлые показатели эффективности не гарантируют будущих результатов.

Участие в розничной торговле уменьшается по наличным деньгам и опционам

Циклы и высокая бета могут означать возврат

Анти-импульс Риск ротации остается высоким

Читать далее здесь...

Тайлер Дерден

Свадьба, 08/13/2025 - 14:40

![Трамп устроил шоу у Белого дома. Навроцкий наблюдал за всем [ВИДЕО]](https://cdn.galleries.smcloud.net/thumbs/gf-4f7H-YAqB-vvDe_donald-trump-15-j.jpg)