Япония запаниковала, когда доходность взрывается, обрежет выпуск сверхдлинных облигаций для успокоения рынка

Один из самых известных современных афоризмов на Уолл-стрит принадлежит главному инвестиционному стратегу Банка Америки Майклу Хартнетту, который десять лет назад мудро сказал, что Рынки перестают паниковать, когда политики начинают паниковать. " Прошлой ночью японские политики, столкнувшись с рекордными долгосрочными ставками и рекордными потерями бумаг на страховых книгах, Наконец-то запаниковал.

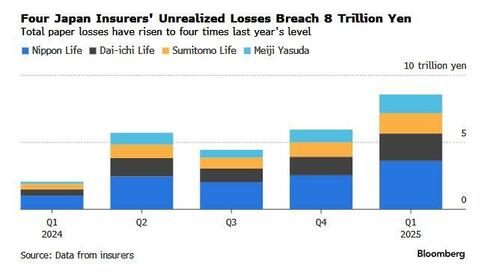

Спустя несколько часов после того, как мы сообщили, что японские компании по страхованию жизни сталкиваются с ошеломляющими потерями.

Сначала Рейтер, а затем Блумберг сообщили (что означает, что это был не «подделка», а преднамеренный пробный воздушный шар Токио, предназначенный для удара по всем основным новостным агентствам), что Япония возьмет страницу прямо из Джанет Йелленс. Активистское казначейство выпустит сценарий и будет «рассматривать» сокращение выпуска сверхдлинных облигаций в связи с недавним резким повышением доходности для банкнот, в попытке устранить устаревшее предложение, которое обрушило цены на долгосрочные облигации до рекордно низкого уровня, поскольку политики стремятся успокоить опасения рынка по поводу ухудшения государственных финансов.

Как и ожидалось, доходность сверхдлинных облигаций упала в отчете, снизив японскую иену и США. Доходность казначейских облигаций на этом пути, поскольку рынки приветствовали готовность Токио остановить всплески долгосрочных процентных ставок, сместив продолжительность с долгосрочного на краткосрочный.

По данным Reuters, Министерство финансов Японии (MOF) рассмотрит вопрос о корректировке состава своей облигационной программы на текущий финансовый год; Это может быть связано с сокращением выпуска сверхдлинных облигаций, сказали источники, которые непосредственно знали о плане. Это очень похоже на то, что Йеллен представила чуть более двух лет назад, когда она перевела большую часть выпуска облигаций с купонов на счета, чтобы продолжать финансировать дефицит США через законопроекты и истощение счета Реверс Репо, который сейчас почти пуст.

MOF примет окончательное решение после обсуждений с участниками рынка в середине-конце июня.

План последовал за недавним рекордным ростом доходности сверхдлинных облигаций до никогда ранее невиданных уровней из-за замораживания спроса со стороны традиционных покупателей, таких как страховщики жизни и глобальный рынок, который колеблется из-за неуклонно растущего уровня долга.

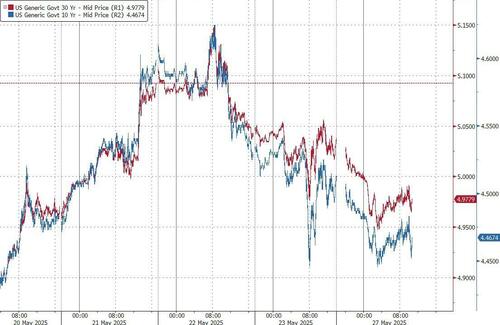

Доходность по 30-летним японским государственным облигациям (JGB) упала на 18 базисных пунктов до 2,85% после отчета, самого низкого уровня с 4 мая. Базовая 10-летняя доходность снизилась на 7 пунктов до 1,43%.

Падение сверхдлинных доходностей JGB также помогло повысить долгосрочные доходности казначейства США, которые были установлены для их крупнейшего однодневного падения с середины апреля. Доходность по 30-летним облигациям снизилась на 7 базисных пунктов на 4,963% в начале торгов в Лондоне во вторник.

"" Мы утверждали, что что-то должно было дать, чтобы исправить дисбаланс спроса и предложения в долгосрочных JGB. Рынок думает, что это будет MOF, - говорится в записке Societe Generale, повторяя то, что мы, в свою очередь, говорили в течение нескольких недель.

По словам источников, если MOF сократит выпуск 20-, 30- или 40-летних JGB, это, скорее всего, увеличит выпуск более коротких долговых обязательств; Таким образом, общий запланированный размер выпуска JGB на текущий финансовый год, который заканчивается в марте 2026 года, останется неизменным с 172,3 трлн иен (1,21 трлн долларов).

Такой шаг также будет означать, что любой предельный спрос на длительность должен будет отправиться в США, которые благодаря большой, красивой, бюджетной сделке Трампа будут иметь. много Долгосрочные поставки на долгие годы.

Глобальные рынки были потрясены резкими распродажами облигаций в последнее время, в том числе для казначейских облигаций США, поскольку широкие тарифы президента Трампа и неустойчивая политика усилили опасения по поводу статуса суверенного долга США как самого безопасного убежища в мире. В Японии сверхдлинные облигации также были распроданы, когда премьер-министр Сигеру Исиба столкнулся с проблемами. Политическое давление на снижение налогов и большие расходы в преддверии опроса верхней палаты в июле. Это может увеличить и без того огромный государственный долг страны.

Правительство Японии рассматривает возможность составления еще одного пакета расходов, хотя руководители правящей коалиции договорились во вторник избегать выпуска новых облигаций с дефицитным финансированием. Столкновение по поводу фискальной политики побудило премьер-министра Японии сказать тихую часть вслух, признав на прошлой неделе, что Финансовое положение Японии было хуже, чем в Греции.

Крах JGB также обратил внимание инвесторов на то, может ли MOF, который контролирует выпуск долгов, и BOJ принять меры для сдерживания роста сверхдлинных доходностей.

Банк Японии, со своей стороны, вряд ли внесет какие-либо большие изменения в свою текущую программу облигаций (или QE), сообщили источники Reuters. Но недавний крах рынка может повлиять на его планы по сокращению бюджета на 2026 финансовый год, которые будут решены на совещании по вопросам политики в следующем месяце.

«Выдача сверхдлинных JGB может снизиться в июле», что ослабит обеспокоенность по поводу результатов 40-летнего аукциона JGB в среду, сказал Кацутоши Инадоме, старший стратег Sumitomo Mitsui Trust Asset Management.

"" Но это лишь временное облегчение и не приведет к снижению долгового баланса Японии. Учитывая, что МВФ, вероятно, выполняет свою роль, политикам теперь необходимо приложить усилия, чтобы избежать увеличения долга. "

Bloomberg сообщает, что в Консультативная группа правительства Японии призвала власти активизировать усилия по бюджетной консолидации. Поскольку продолжающиеся усилия Банка Японии по ужесточению денежно-кредитной политики повышают риск более высоких затрат на обслуживание долга для самой развитой страны мира с задолженностью.

Совет по фискальной системе предупредил, что Повышение процентных ставок Банка Японии и сокращение покупок облигаций подпитывают устойчивый рост доходности государственных облигаций, Финансы страны требуют большего внимания, согласно предложению, представленному министру финансов Катсунобу Като во вторник.

«Мы должны управлять финансами с повышенным чувством срочности, чтобы предотвратить рост долговых расходов от вытеснения основных политических расходов», — говорится в заявлении. Призыв к фискальной осмотрительности прозвучал, когда Банк Японии продолжает раскручивать свою ультра-свободную политику после первого повышения процентных ставок за 18 лет в марте прошлого года.

Комиссия предупредила, что Япония может столкнуться с понижением суверенного кредитного рейтинга, если фискальная дисциплина продолжит разрушаться.

"" Понижение государственных облигаций не является надуманным сценарием, - говорится в предложении, ссылаясь на недавнее понижение суверенного долга США Moody's Ratings в качестве прецедента. «Если доверие к государственным финансам Японии ослабнет, это может спровоцировать понижение, резкое повышение процентных ставок, рыночные потрясения и в конечном итоге негативные последствия для домашних хозяйств и предприятий,- сказал он.

** **

Комментируя пробный шар MOF, глава Goldman EMEA Delta-One Рич Привороцкий сказал, что японская стратегия будет краткосрочной полезной.Но если это долгосрочное решение, то проблема будет в валюте. "

Конечно, иена, которая, наконец, показала рекордно длительное воздействие хедж-фондов, падает, и Привороцкий перечисляет следующие причины слабости валюты:

- Выходы механически опускаются в конце кривой, сжимая дифференциалы выходов

- Больше долгов будет принадлежать внутреннему населению, следовательно, меньше спроса на иены.

- Невозможность продать долг, как правило, не является хорошей вещью, поскольку больший процент принадлежит вашему банку.

Вывод Приво заключается в том, что пока он остается "Небольшой шаг для JPY... Стоит, но стоит посмотреть, станет ли это темой за пределами США, в результате рекордного количества долларовых шорт в последнее время. "

Тайлер Дерден

Туэ, 05/27/2025 - 11:25