Цены производителей в США растут самыми быстрыми темпами за 12 месяцев, а Уолл-стрит реагирует

В преддверии завтрашнего ИПЦ трейдеры смотрят на цены производителей этого утра на любые намеки на то, что тенденция к дезинфляции вернется или нет.

Ответ: «Нет!»

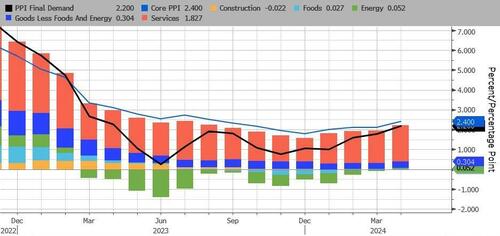

Апрельские цены производителей выросли на 0,5% MoM (против +0,3% exp), С мартовским +0,2% MoM пересмотрен до -0,1% MoM. Пересмотр в сторону понижения не остановил рост индекса YoY до 2,2% (с +2,1% в марте).

Источник: Bloomberg

Это самый высокий показатель с апреля 2023 года и является четверкой самых горячих, чем ожидалось, заголовков PPI.

Источник: Bloomberg

Цены производителей были агрессивно пересмотрены в течение 4 из последних 7 месяцев.

Источник: Bloomberg

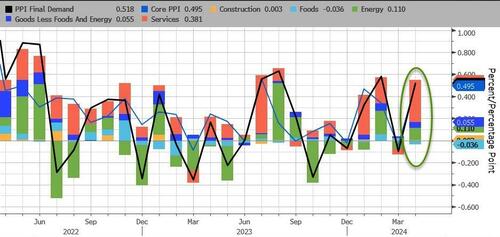

Расходы на услуги выросли, Доминирование ИПП в апреле с энергетикой является вторым по важности фактором. Цены на продукты питания фактически снизились на бас-гитаре MoM.

Источник: Bloomberg

На бас-гитаре YoY, в росте индекса PPI доминировали сервисы (рост на самом жарком уровне с июля 2023 года). Впервые с февраля 2023 года ни один из основных факторов не был отрицательным на базе YY.

Источник: Bloomberg

После случайно скорректированной цены на бензин в прошлом месяце В апреле индекс PPI Gasoline вырос (с реальными ценами на насос), но ему еще предстоит пройти долгий путь.

Источник: Bloomberg

Основной индекс PPI был снижен - рост на 0,5% (более чем в два раза выше ожидаемого + 0,2%). - что подтолкнуло Core PPI YoY до +2,4%.

Источник: Bloomberg

И, наконец, окончательный спрос на энергоресурсы и торговые услуги в США вырос на 0,4% и 3,1% в годовом исчислении (самый высокий за 12 месяцев).

Хуже того, трубопровод для первичного ИЦП не очень хорош, так как промежуточный спрос начинает ускоряться.

Источник: Bloomberg

Вот реакция Уолл-стрит на PPI:

Крис Ларкин (Chris Larkin) из Morgan Stanley

Прилипкая инфляция выглядела сегодня утром после гораздо более горячей, чем вымершая инфляция. Но с учетом того, что в прошлом месяце цифры были пересмотрены ниже, этот отчет, возможно, не был таким большим шоком, как казалось раньше.

Верно это или нет, но тенденции ИПЦ оказывают большее краткосрочное влияние на рынки, поэтому картина может сильно отличаться через 24 часа. Но если ИПЦ также превзойдет ожидания, интересующая картина процентных ставок может быть в три раза больше.

Инвестиции на заказ Группа:

Результаты апрельского ИПП показали более горячее, чем ожидалось, чтение м/м. Это плохая новость. Тем не менее, показания были намного ближе к ожиданиям, поскольку мартовский отчет был пересмотрен до отрицательных 0,1% как на заголовке, так и на основном бас-гитаре. "

Крис Заккарелли из Independent Advisor Alliance

Эта неделя важна для рынков, потому что они приветствуют инфляцию, и утренний индекс цен производителей не сделал ничего, чтобы помочь этим страхам.

Наиболее важным выпуском данных является завтрашняя печать ИПЦ, потому что двойной мандат ФРС основан на ИПЦ и безработице, причем первый является тем, на чем ФРС сосредоточена исключительно сейчас.

Мы считаем, что фондовый рынок будет расти в течение года на сильных корпоративных прибылях и потребительских расходах, но гибкость, скорее всего, привлечет средства, потому что данные по инфляции будут держать ФРС на грани.

Куинси Кросби из LPL Financial:

Кроме того, в этом докладе подчеркивается ФРС считает, что путь дезинфляции стал более жестким, требуя более длительной политики для борьбы с, казалось бы, введенной инфляцией.

Главный вопрос — и мощная дилемма — заключается в том, смягчается ли экономический ландшафт вещателя, в то же время инфляция на дюйм выше, что делает работу ФРС творчески трудной.

Билл Адамс из Comerica Bank

Между повышательным сюрпризом и понижательным пересмотром к предыдущей дате тенденция в общем ИПП была немного выше, чем ожидалось в апреле.

Отчет PPI предполагает повышенный риск для апрельского отчета CPI, который выйдет завтра.

На марже ФРС будет рассматривать отчет PPI как еще одну причину замедления снижения процентных ставок.

Пол Эшворт из Capital Economics:

В наши дни мы в основном заботимся о том, что PPI означает для предпочтительного дефлятора PCE ФРС показателя базовой инфляции потребительских цен.

В этом отношении апрельские новости были неоднозначными, но, в целом, огорчающими. Плохая новость заключается в том, что цены на управление портфелем PPI выросли на 3,9%. Но это было более чем преувеличено хорошей новостью. Мы узнаем больше после выпуска апрельского индекса потребительских цен завтра.

Скотт Хелфштейн из Global X:

Инфляция и ФРС менее важны, чем рост, и компании обновились к новой реальности более высоких цен и продолжают искать технологические решения для управления прибылью.

Последняя миля инфляции всегда была самой трудной, но мы должны быть довольны этими цифрами.

За последний месяц «более высокие цены» доминировали над «более низкими ценами» в последних данных опроса.

Более высокие цены производителей:

- Стоимость производства в Нью-Йоркской империи выросла с 28,7 до 33,7.

- Филадельфия Производители ФРС сообщили, что цены, уплаченные в марте, выросли до 23,0 с 3,7.

- Филадельфия Непроизводственные цены ФРС выросли до 31,0 с 26,6 в предыдущем месяце.

- Ричмонд Цены на услуги ФРС выросли до 6,11 с 5,43 в марте.

- Канзас-Сити Цены на производство ФРС повысились до 18 с 17.

- Канзас-Сити Рост цен на услуги ФРС продолжал опережать цены продажи.

- S&P Глобальная инфляция затрат на производство ускорилась, чтобы намекнуть на устойчивое в краткосрочной перспективе повышательное давление на цены продажи.

- ИСМ Выплаченные цены на производство выросли до 60,9, что является самым высоким показателем с июня 2022 года, с 55,7 в марте.

- ИСМ Цены на услуги выросли до 59,2, что является самым высоким показателем с января, с 53,4 в марте.

Снижение цен производителей:

- Цены на услуги ФРС в Нью-Йорке упали до 53,4 с 55,1 в марте.

- Ричмонд Темпы роста производства ФРС по уплаченным ценам распределились до 2,79 с 3,22 в марте

- Согласно прогнозу Dallas Fed Manufacturing, цены на сырье упали до 11,2 с 21,1 в предыдущем месяце.

- Индекс цен на услуги в Далласе снизился до 28,8 с 30,4 в предыдущем месяце.

- S&P Global Service Затраты на производство пилы выросли с шестимесячных максимумов в марте.

Ты видишь сейчас "фляцию", Джей?

Таким образом, нет, ФРС не контролирует инфляцию.

Тайлер Дерден

Туэ, 05/14/2024 - 8:43