Рекордный долг домохозяйств, прыжок в Delinquencias сигнал «ухудшение финансового кризиса», ФРС предупреждает

В то время как рынок вновь фокусируется на завтрашней печати индекса потребительских цен, и в меньшей степени на апрельских отчетах о розничных продажах, которые должны быть представлены в 8:30 утра 15 мая. Мы должны отметить еще один репрезентативный отчет, который обычно не привлекает большого внимания: только что опубликованный отчет по долгу и кредиту домохозяйств ФРС Нью-Йорка за 1 квартал 2024 года, в котором более поздние данные о задолженности по кредитным картам и правонарушениях заняли самую важную часть отчета.

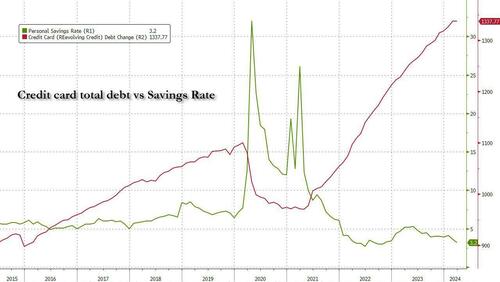

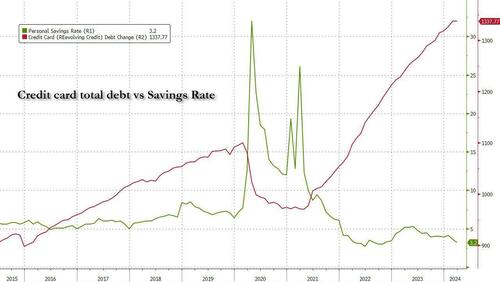

Хотя мы уже знаем, что в последний месяц марта, Общий потребительский долг достиг рекордно высокого уровня (несмотря на резкое замедление роста кредитных карт), даже когда ставка личных сбережений была подключена к рекордно низкому уровню.Едва ли это звучит как одобрение для ряда потребителей США.

Сегодняшний отчет предоставил более детальные детали, которые, однако, не изменили вывод: американский потребитель становится слабее, и, хотя он еще не находится в кризисе, он достигнет этого достаточно скоро.

Как видно из графика ФРС Нью-Йорка, в конце первого квартала долг домохозяйств США стал рекордным, и все больше неимущих борются за то, чтобы не отставать: общий долг домохозяйств США вырос до 17,69 триллиона долларов, говорится в квартальном отчете NYFed о долге и кредитах домохозяйств. Это увеличение на 184 миллиарда долларов, или 1,1%, по сравнению с четырьмя кварталами.

Потребители добавили 3,4 триллиона долларов долга после пандемии, и это увеличение долга несет гораздо более высокие процентные ставки.

И как с кредитными картами, так и с полным кредитом на все времена, Данные искажают растущее финансовое давление на американские семьи в эпоху выбранной инфляции.. Постоянный рост цен на предметы первой необходимости, такие как еда и рента, сохранил бюджеты домашних хозяйств, заставляя людей платить по кредитным картам.

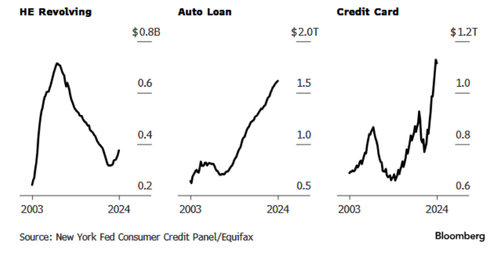

Общий дебет по кредитным картам составил $1,12 трлн в первом квартале 2024 года, согласно отчету (число отличается от ежемесячной печати, сообщенной на прошлой неделе ФРС Нью-Йорка и которая была намного выше), но Все больше братьев отстают в платежах по кредитным картам. Несмотря на то, что в соответствии с этим набором данных (если не другим набором данных ФРС Нью-Йорка) этот показатель несколько снизился, количество в соответствии с сезонными моделями потребителей, оплачивающих дебет, вошло в праздничные дни. Но, как отмечает Bloomberg, остатки по кредитным картам выросли максимум на 25% по сравнению с первым кварталом 2020 года.

Балансы по кредитным картам полезно растут во втором и третьем кварталах, а затем они действительно имеют тенденцию оживлять праздники в 4 квартале. Тед Россман, старший аналитик Bankrate, пишет в записке для клиентов. "С инфляцией и процентными ставками, которые, вероятно, останутся повышенными, есть очень хороший шанс, что остатки по кредитным картам достигнут новых высот в 2024 году. "

Между тем, в блоге экономистов ФРС Нью-Йорка они написали, что "Потребители, столкнувшиеся с финансовым давлением, могут максимизировать свои кредитные карты и отстать от платежей.Один наблюдаемый фактор, который сильно коррелирует с будущими делинкенциями, - это высокий коэффициент использования кредитных карт. "

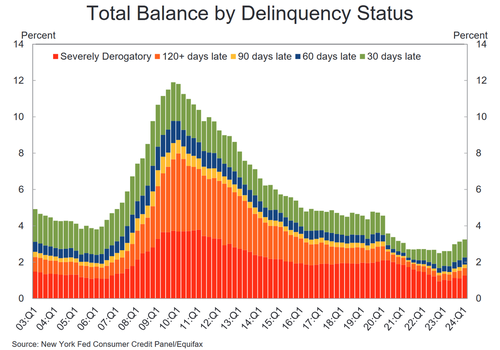

«В первом квартале 2024 года ставки по кредитным картам и автокредитам в случае серьезных правонарушений продолжали расти во всех возрастных группах», - сказала Жоэль Скалли, региональный экономический директор в Отделе исследований домохозяйств и государственной политики ФРС Нью-Йорка.. «Все большее число заемщиков пропустили платежи по кредитным картам, что свидетельствует об ухудшении финансового положения некоторых домов. "

По состоянию на март 3,2% внешнего долга находилось на той или иной стадии правонарушений. Это по-прежнему на 1,5% ниже, чем в четвертом квартале 2019 года, но показатели переходного периода увеличились для всех типов продуктов. А также заинтересованные ставки до covid были примерно на 5% ниже.

В отдельном посте экономисты ФРС Сент-Луиса отметили, что уровень преступности по кредитным картам возвращается к исторически более нормальным уровням после того, как программы государственной помощи, связанные с пандемией, подтолкнули их к уникально низким цифрам. Вместе с тем они добавили, что "нынешние уровни преступности, связанной с кредитными картами, значительно превышают уровни, существовавшие до пандемии, что говорит о том, что тенденция, начавшаяся до пандемии, ускорилась. "

Около 121 000 потребителей добавили нотацию о банкротстве в свои кредитные отчеты в прошлом квартале, и примерно 4,8% потребителей слышали меньше в сторонних коллекциях. Что примечательно, так это то, что эти потребители в настоящее время в сборе имеют наибольшее количество в рекордных количествах. Это означает, что как только поезд по борьбе с преступностью наконец покинет станцию, а кредиторы начнут собирать средства на прослушивание, сумма долга в 3-й партийной коллекции будет буквально зашкаливать!

И самый ясный намек, что мы туда попадаем, Дело в том, что заемщики, использующие более 60% своих кредитов, впадают в преступность быстрыми темпами, чем до пандемии. Это составляет большую часть увеличения ставок по просроченным кредитным картам. По поводу Треть остатков средств, связанных с неимущими, использующими более 90% своего кредита, стали просроченными в прошлом году, в сочетании с примерно 25% до пандемии.

![]()

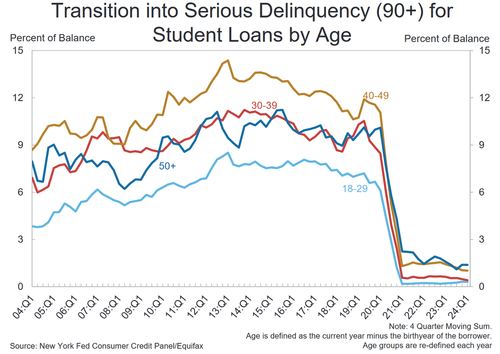

Самое примечательное здесь то, что, несмотря на так называемый конец моратория на выплату студенческого кредита, кажется, что не только никто не погашает свои студенческие кредиты, но и проблемы с задолженностью. Даже не замужем, чтобы сделать просроченный долг как таковой.Опять же, трудно определить, какая часть этого долга является просроченной, поскольку просроченные федеральные платежи по студенческим кредитам не будут сообщаться в кредитные бюро до четырех кварталов.

Данные также показывают широкий диапазон ставок использования кредитных карт. Каждый шестой пользователь кредитной карты использует не менее 90% доступного кредита.. Еще 11% используют от 60% до 90% доступного кредита.

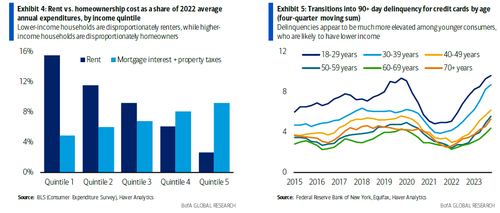

Исследователи ФРС обнаружили, что молодые братья и те, у кого более низкие доходы, более склонны к финансовому стрессу, чем пожилые люди и те, у кого более высокие доходы, у которых может быть больше кредитов. "Тысячелетия были единственной группой, у которой делинкенции превышали допандемический уровень.Исследователи ФРС Нью-Йорка возвращаются в блоге.

В отчете ФРС показано, что 6,9% дебетовых кредитных карт перешли на серьезные правонарушения в прошлом квартале, по сравнению с 4,6% год назад. А для держателей кредитных карт в возрасте 18-29 лет 9,9% остатков были серьезными правонарушениями.

![]()

Кредитные просрочки также выше, так как средний ежемесячный платеж за автомобиль подскочил до 738 долларов в 2023 году. Около 2,8% автозалов теперь 90 или более дней просрочены, что составляет более 3 миллионов автомобилей.. Автокредиты являются второй по величине долговой категорией после ипотечного долга с непогашенными $1,62 трлн.

Самая большая задолженность домохозяйств - за жилье. Это составляет более 70% от общего числа. Этот долг работает хорошо, но домовладельцы активно подделывают свой накопленный домашний капитал в виде ипотечных кредитов, в то время как новые источники ипотеки упали почти на рекордно низком уровне в результате высоких ставок.

... что также означает, что выкупы начинают тикать.

Между тем, по другую сторону таблицы первоначально было выделено около 16 миллиардов долларов дополнительных кредитов на собственный капитал - самый большой рост с 2008 года - и 37 миллиардов долларов было добавлено за последний год. У домовладельцев есть около 580 миллиардов долларов внешнего кредита собственного капитала, самого большого примерно за 15 лет.

Так что же делать с этой информацией, особенно когда даже ФРС предупреждает, что американский потребитель находится в творчески слабой доле.

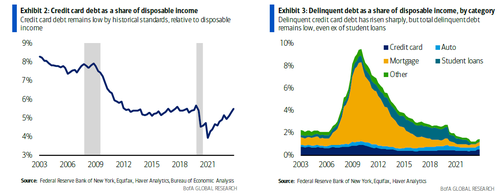

Задолженность по кредитным картам резко увеличилась в последние кварталы. Когда в 2 квартале 2023 года он впервые в истории превысил 1,0 трлн долларов, в некоторых кругах даже по мнению экономистов Bank of America (особенно сангиных), хирург по дебету кредитных карт частично является стандартизацией после того, как потребители использовали свои финансовые стимулы для погашения своих остатков в 2020-21 годах. Более того, они отмечают, что даже если оставить в стороне структурный отход от наличных денег, дебет по кредитным картам должен увеличиться с номинальной экономикой. В качестве доли располагаемого дохода общий дебет по кредитным картам в 4 квартале 2023 года все еще был ниже допандемического уровня.

Вместо общего кредитного номера BofA призывает клиентов уделять больше внимания делинкенциям кредитных карт: общая сумма дебетовых акций просроченных кредитных карт в размере 110 млрд долларов США по состоянию на 4 квартал 2023 года, что на 42% выше; это число еще выше в 1 квартале 2024 года.

Чтобы представить эти цифры в контексте, BofA предлагает два подхода: Почему вы не должны слишком беспокоиться

- Насколько рост делинквенций повлияет на потребительские расходы? Хорошей новостью является то, что кредитные карты составляют всего 6,5% от общего потребительского долга. Несмотря на недавнее увеличение, просроченный дебет по кредитным картам составляет всего 0,5% от общего неблагополучного дохода.

- Между тем, ипотечные кредиты составляют 70% потребительского дебета и, безусловно, являются самым большим фактором колебаний для общих просрочек. Большая часть домов заперта в низкой фиксированной ставке 30-летней ипотеки. Это сохранило ипотечные просрочки и общий просроченный долг, очень низкий по историческим стандартам, и сделало потребительские расходы более резидентными, чем в прошлом.. Даже когда студенческий кредит, наконец, нормализуется, это не приведет к необходимости многого, если ипотечный долг восстановит таблицу.

И вот почему вы должны беспокоиться:

- Пока так хорошо, но картина получает немного больше концерта в нижней части распределения доходов. Дома с низким доходом менее склонны быть домовладельцами. Таким образом, они получают меньшую выгоду от низких фиксированных ставок по ипотечным кредитам. Между тем, они, скорее всего, также будут несостоятельными по своим кредитным картам. Из этого факта можно сделать вывод, что Преступления по кредитным картам, по-видимому, выше среди молодых потребителей (которые в среднем имеют более низкий доход).

- Кроме того, delinquencias может занижать проблемы, которые потребители делают из-за дебета кредитной карты. Вероятно, существует большая группа потребителей, которые платят свои минимальные остатки, и поэтому не являются правонарушителями, но не могут оплатить весь остаток.И поэтому платят высокие APR на просроченные суммы. АТР значительно выросли из-за повышения ФРС, IncОблегчение улиц для таких потребителей.

Подробнее в полной записке BofA доступно для профессиональных подписчиков.

Тайлер Дерден

Тюэ, 05/14/2024 - 18:00