Обсуждение Hawk Down

Бенджамин Пиктон, старший макростратег Rabobank

Облигации были распроданы в пятницу, а NASDAQ закрылся ниже. Как S&P500, так и Dow Jones добились незначительного прироста, при этом показатели Dow не позволяют предположить, что акции продолжают торговаться с чувствительностью к ставкам дисконтирования. Двухлетние годы выросли на 3bps в пятницу, в то время как 10-летние управляли приростом на 4.7bps, управляя кривой медведя.

Нефть Brent торгуется чуть выше пятничного закрытия в 83,98 доллара за баррель, несмотря на новости в минувшие выходные о том, что президент Ирана Эбрахим Раиси пропал без вести после того, как вертолет с министром иностранных дел Амирабдоллахианом треснул в горной местности на северо-западе страны. Последние сообщения свидетельствуют о том, что обломки были обнаружены поисковыми группами, но никаких признаков жизни пока не обнаружено.

Хотя нет никаких предположений о нечестной игре, совершенно не идеально, чтобы высокопоставленные иранские политические деятели участвовали в поставках вертолетов, в то время как давление между Израилем и Ираном остается повышенным. Экономист предположил, что если Раиси будет убит, это может спровоцировать борьбу за власть в Иране, поскольку он был ведущим кандидатом, чтобы стать окончательным успехом для Верховного лидера Хамейни.. Тем не менее, реакция в энергокомплексе предполагает, что трейдеры восстанавливают неспокойные новости.

Сдвиг - интересный мир ставок, Юбилей после КПИ явно начал ослабевать в конце прошлой недели, когда ряд спикеров ФРС по очереди поливали проверенную чашу для пунша.. Местер, Уильямс и Баркин обсудили перспективы снижения ставок, предположив, что возможно, возможно, будет целесообразно снизить ставки до конца года. Или нет.

Местер, один из наиболее ястребиных членов FOMC, уйдет в отставку в конце июня. Она набрала +1 по спектрометру «ястреб/голубь» Bloomberg Economics. В соответствии с текущим составом FOMC спектрометр сводится к нулю (ни ястребиный, ни голубоватый). Это означает, что приглашающий президент ФРС Кливленда, который вернет себе члена с правом голоса в 2024 и 2025 годах, может склонить ФРС к общей предвзятости в любом направлении.

Между тем, Боуман (возможно, член FOMCs Bridge Hawkish) сказала, что прогресс на перебалансировке рынка труда замедлился, ФРС отслеживает, эффективно ли возрождается политика, и она готова снова подняться, если инфляция начнет расти.

Мы могли бы взять с собой спикеров ФРС для подготовки предварительных прогнозов будущего снижения ставок в оговорках о потенциале роста инфляции. На прошлой неделе CPI, хотя и приветствуется, был первым релизом за три месяца, который не удивил. После того, как поворотное лето Пауэлла в прошлом году вызвало бешеную спецификацию сроков и кванта сокращений ставок, он видит только цель быть немного более осмотрительным на этот раз, когда данные падают на пути ФРС.

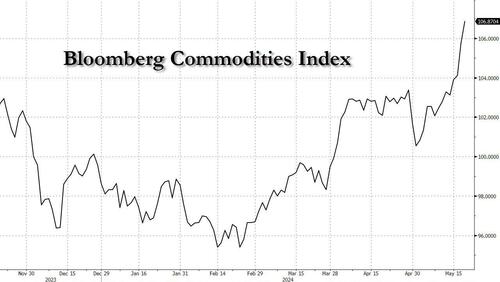

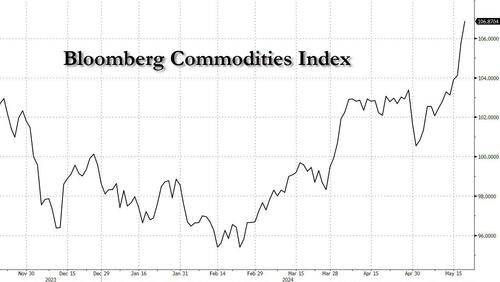

Действительно, Индекс сообществ Bloomberg предупреждает, что пока не следует писать некролог инфляции. Он падает с февраля и сейчас находится на самом высоком уровне с октября прошлого года. Какао постоянно отступает с апрельских максимумов, как и хлопок, сахар и кофе. Но они были более чем компенсированы недавними пробежками в алюминии, никеле, меди, серебре, железной руде, стали, апельсиновом соке, соевых бобах, пшенице, говядине, золоте, природном газе и дизельном топливе., В то время как недавний запрет на импорт интегрированного урана из России также может усилить ценовое давление в цепочке поставок ядерного топлива.. Более высокие цены на коммунальные услуги, как известно, бесполезны, в то время как инфляция основных услуг восстанавливает проблему.

В целом, Похоже, что мы снова «ждем больше данных» на данный момент, но майские протоколы заседания FOMC, которые должны выйти на этой неделе, по-прежнему будут ключевым моментом для рынков.

Резервный банк Новой Зеландии будет еще одной точкой интереса, поскольку он собирается установить официальную ставку наличности. От преобладающих 5,50% изменений не ожидается, но запланированный выпуск Заявления о денежно-кредитной политике, которое включает обновленные прогнозы, будет иметь важное значение для местного рынка.

RBNZ зарекомендовал себя как нечто вроде «погоды» для глобальных циклов процентных ставок. Учитывая, что экономика находится в рецессии, а рынок труда демонстрирует недавние признаки быстрого смягчения, стоит обратить внимание на то, как RCNZ отмечает возможность более раннего снижения ставки, чем их нынешнее руководство к середине 2025 года.

Протокол майского заседания РБА также должен быть опубликован на этой неделе и может стать точкой контраста. В то время как РБНЗ обладает роскошью фокусироваться на инфляции, РБА должен согласовать свою цель стабильности цен с мандатом полной занятости. Это явно идет в направлении изучения отсутствия какого-либо ястребиного наклона от RBA в мае, даже несмотря на то, что данные по инфляции в 1 квартале и рынку труда до встречи были удивительными.

Как однажды сказал Леонард Нимой:Если вы будете преследовать двух кроликов, вы потеряете их обоих.Все в порядке. "

Тайлер Дерден

Mon, 05/20/2024 - 12:20