«Потерянный контроль» — сюрприз дефицита бюджета Великобритании Баттерс Стерлинг

Финансовый фарс в Великобритании сегодня утром пошел от плохого к худшему, поскольку государственные заимствования оказались значительно выше, чем прогнозировалось в августе.

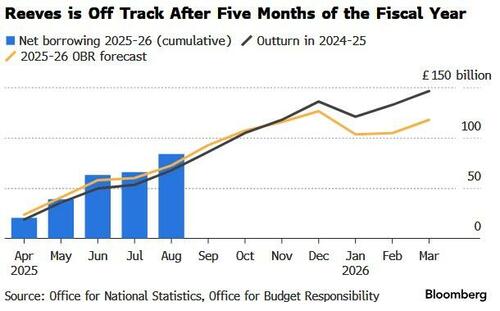

Еще одним ударом по канцлеру казначейства Рейчел Ривз - перед сложным бюджетом осенью (осенью) - Дефицит составил £18 млрд ($24,4 млрд), сообщило Управление национальной статистики в пятницу. намного выше 12,5 млрд фунтов стерлингов, прогнозировало Управление по бюджетной ответственности. Самый высокий уровень заимствований за месяц за пять лет.

Источник: Bloomberg

Как сообщает Bloomberg, это оставило дефицит после пяти месяцев финансового года на уровне 83,8 млрд фунтов стерлингов - на 11,4 млрд фунтов стерлингов выше прогноза OBR. Это второй по величине показатель с 1993 года после пандемии в 2020 году. Дефицит составил 67,6 млрд фунтов годом ранее.

Источник: Bloomberg

Неутешительные августовские цифры были дополнены серией пересмотров предыдущих четырех месяцев. Это добавило к дефициту 5,9 млрд фунтов стерлингов, в основном из-за более низких, чем предполагалось ранее, поступлений от НДС и более высоких расходов и заимствований местного правительства.

Ривз посмотрел на трассу в этом году С более сильными налоговыми поступлениями, компенсирующими более высокие расходы, но последние цифры являются значительным препятствием, подчеркивая опасное состояние государственных финансов и потенциально дальнейшее разрушение небольшого запаса в 9,9 млрд фунтов стерлингов, выделенного против ее основного фискального правила.

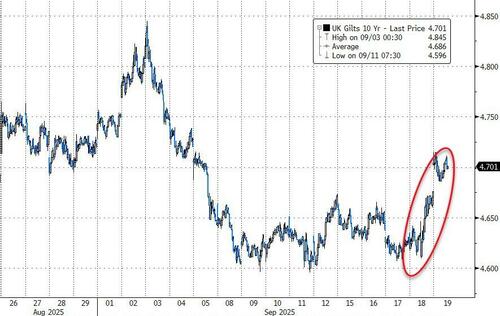

Фунт и позолота упали.

Доходность 10-летних облигаций выросла на два базисных пункта до 4,70%, а 30-летняя ставка выросла на три базисных пункта до 5,54%.

Источник: Bloomberg

Стерлинг упал на 0,5% до $1,3483, что является самым низким показателем с 8 сентября.

Источник: Bloomberg

Канцлер потерял контроль над государственными финансами. Мел Страйд, оппозиционный консервативный теневой канцлер, сказал.

Ривз уже столкнулась с трудным бюджетом 26 ноября, когда она, как ожидается, объявит о повышении налогов на миллиарды фунтов, чтобы компенсировать более высокие затраты по займам, политические изменения и ожидаемое снижение роста OBR.

Джеймс Мюррей, главный секретарь Казначейства, сказал: «У правительства есть план» Снизить заимствования, потому что деньги налогоплательщиков должны быть потрачены на приоритеты страны, а не на долговые проценты. "

Bloomberg Economics считает, что для покрытия долгового разрыва необходимо 35 млрд фунтов Об этом стало известно после весеннего заявления.

Тайлер Дерден

Фри, 09/19/2025 - 08:40